Throughout 2023, the conversation around artificial intelligence (AI) has permeated all aspects of our society. Insurers have not been immune from these discussions. Datos Insights’ direct experience is that the understanding of AI topics among C-level insurer executives has matured dramatically in recent months. Insurers are increasingly trying to get more specifics on how AI will impact the broader insurance industry and their specific lines of business.

Large language models (LLMs) have been a source of particular interest and confusion. In conversations with Datos Insights, insurance technology executives express a spectrum of views on these tools, ranging from questioning whether an insurer should build LLMs to questioning if LLM capabilities have any value whatsoever.

This report, sponsored by DXC Technology and written by Datos Insights, provides basic definitions of various language models and explores how insurers will most likely utilize LLMs. Additionally, the report presents a decision table outlining factors that insurers can consider as they contemplate various options to determine reasonable courses of action while avoiding expensive and unrealistic choices that do not create value.

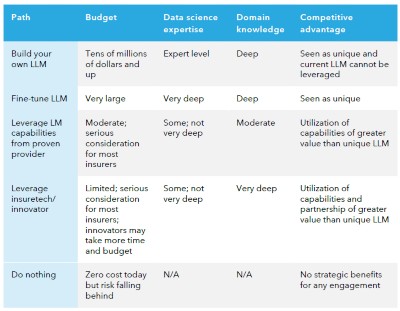

Decision Table

Table A summarizes the five paths for insurers looking to engage with language models discussed in this paper. The columns capture four different strategic parameters: budget, insurer data science expertise, insurance domain knowledge, and competitive advantage.

Table A: Language Model Decision Paths

Source: Datos Insights

Insurers should start with their budget. Cost is a significant matter that is sometimes overlooked. Although public data is not perfect, there is general agreement that LLM development is very expensive. SLMs may mitigate this. All AI endeavors must have consideration for the financial resources an insurer has to invest.

Available data science expertise will determine which options an insurer can effectively execute. The range of data science expertise in insurance ranges tremendously. Some very large insurers have invested significantly in data science teams with expertise that rivals organizations in any vertical. Other companies are far more limited, and their data investments to date may be more centered on operational reporting, dashboards, and other tactical investments. As insurers consider these options, they must be candid about the current state of their data science capabilities.

Insurance domain knowledge is also a key decision parameter. Of course, insurers commonly (though not universally) have deep domain knowledge about their own data. However, whether those resources can be freed up for significant time investments is an issue. Even if the resources are available, AI requires new skills and approaches, and resources with deep domain knowledge may not be able to learn the new skillset.

Conclusion

Insurers of all sizes are talking about language models — and they should be. Insurance leaders must understand these concepts to set technology direction, participate in industry conversations, understand regulatory impacts, and engage across their organizations, including with board members.

Most insurers, but not all, are likely to leverage the power of language models through partners. Those partners may implement capabilities via LLMs or SLMs.

Insurers should continue to closely monitor developments in generative AI, especially in SLMs, as strategic decisions that hinge on cost and time spent training LLMs may be evaluated differently as SLM capabilities improve and become more widely available.