A paper by DXC Leading Edge

A Great Transition is underway. The guiding principles of the economy, derived from the Industrial Revolution, are being overturned:

- First, the principal basis of wealth creation has shifted, from using physical assets to transform natural resources, to exploiting intangible assets based on information.

- Second, beliefs about what matters are undergoing change, with a shift from value to values, often labelled environmental, social and governance (ESG).

- Third, a transformation is occurring in the structure of work, with a move away from offices, fixed employment and set working hours to more flexible patterns.

Taken together, these forces form a Great Transition* to a new economic model that in many ways represents not a continuation of the Industrial Revolution — a Fourth Industrial Revolution — but a return to the principles that prevailed beforehand. What are the implications of the new model for enterprises? What does it take to succeed in this new world?

How businesses create value: From a material economy to an information economy based on intangible assets

Prior to the Industrial Revolution, land was the dominant form of capital. The economy was organic and circular. Then came coal, steam and machinery, which were harnessed to convert physical material into physical products.

Today, a comparable transition is well underway to a qualitatively different economy, where intangible assets are the principal means of creating value. Intangible assets are united by the common thread of information, whether in the form of data, software, intellectual property or brands. Energy is used to create and process information instead of physical material.

Intangible assets outweigh tangible assets against every significant economic metric: capital, investment, returns, productivity and employment.

With the advent of the intangible economy, industry does not go away. However, it is in the intangible domain that value is increasingly created. Information, once an adjunct to products and services, has now become the most valuable product and service.

With the advent of the intangible economy, industry does not go away. However, it is in the intangible domain that value is increasingly created. Information, once an adjunct to products and services, has now become the most valuable product and service.

Intangible assets change the rules of the game

Intangible assets have several important characteristics:

Scale. Whereas physical assets wear out, intangibles scale without decreasing in value. When costs do not rise directly in proportion to revenues, the focus of any business naturally shifts to achieving scale and maximizing revenue.

Sustainability. The intangible economy is inherently more sustainable since intangible assets do not depend on the depletion of natural resources.

Wealth. Because the information economy creates wealth and jobs, it becomes feasible at a macroeconomic level for there to be a transition away from industry.

Expertise. As information comes to play an ever-greater role in the economy, the importance increases of the ultimate general-purpose information processor: the human brain. Since intangible assets are conceived, designed and built by people, there is a premium to be paid for highly skilled workers.

The purpose of business: From value to values

During the 17th and 18th centuries, first in The Netherlands and then in England, priorities began to shift from the spiritual to the material. An industrious revolution created a demand pull, where people worked longer hours and sought employment for hard cash to buy populuxe items, such as tea, coffee and cotton fabrics. Thus, the Industrial Revolution was preceded by, and then deepened, a transition in beliefs from values to value.

Today, we are seeing a comparable transition. Only this time it is a reversal of the Industrial Revolution. We are moving back from economic value alone to values. ESG is the term that has come to capture this new set of values. Pressure to place more weight on ESG is coming from all sides: shareholders, customers, employees and governments or regulators.

In ESG thinking, how firms do business matters as much as why, although often this is a false choice. Studies show that firms that are more sustainable, more diverse and have greater employee engagement deliver higher long-run returns.

ESG entails profound transformation at every level:

- Harnessing organic energy. Shifting to sustainable sources of energy is necessary, but far from sufficient.

- Shifting to a circular economy. The industrial economy was linear, from the extraction of resources to the dumping of products. ESG entails a circular model based on re-use and recycling, starting with design and across operations and the supply chain.

- Escaping the ESG trap. There is a risk that firms reap all the downside of compliance box-ticking, and none of the upside of revenue from ESG products and services.

- Adopting a risk rather than cost mindset. In the industrial economy, firms optimized for efficiency. An ESG mindset will place greater weight on risks, expanding both the time horizon and the aperture of its outlook.

Ultimately, delivering these changes entails embedding ESG right across processes, governance and culture.

Ultimately, delivering these changes entails embedding ESG right across processes, governance and culture.

The structure of work: From a single model of work to hybrid working patterns

In the Great Transition we are seeing a fundamental transformation in working patterns, though it is in many respects a return to the model that predated the Industrial Revolution — a model that was marked by piece work, working from home, and multiple jobs and employers.

First, the location of work is moving back to the home. It is hard to determine what the new normal will be after the worst of the pandemic is over, but a survey of HR managers at the end of 2020 found that 26.7% of American workers were expected to work permanently from home. In addition to this shift towards full-time home working, there are countless shades of grey between working in the office and at home. Each firm is seeking the right balance.

Second, there is greater flexibility in working hours. Even the five-day week is coming under scrutiny with experiments of a four-day week in Iceland and the UK, under the principle of 100:80:100: 100% of the pay for 80% of the time, in exchange for maintaining at least 100% productivity.

Third, the traditional employment model, where you either work full time for a single employer or are unemployed, is being eroded. Estimates of the number of people participating in the gig economy are as high as 20% – 30% in 2016.

Across working patterns, the old model of a single employer, a single location and a standard set of hours is not being superseded by a single alternative new model. Instead, the new normal that is emerging is a hybrid, where individuals and enterprises adopt a mixture of working patterns.

A paradigm shift: From Industrial Revolution to Great Transition

The evidence for the Great Transition is all around us. So, why can’t people see and, therefore, react to the transition? It all comes down to paradigms. Like an Escher optical illusion, two people can look at the same picture and see completely different things. The problem is that the dominant paradigm remains that of the industrial era, even though this does not reflect how value is created, nor how, where and why much work gets done.

However, adopting a new paradigm is immensely challenging. Under the old paradigm some things will just not compute: If you focus on ESG as well as economic value, how can this create more economic value? If people work 4 days per week, how can they possibly produce the same as when they work 5 days?

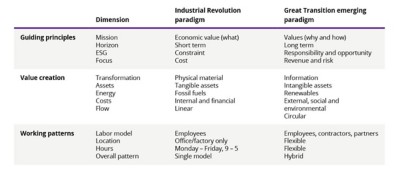

The Great Transition requires a paradigm shift across each of these fundamental dimensions of the economy. See Table 1.

Once leaders shift to the new paradigm, seeing the alternative view in Escher’s optical illusion, they will quickly conclude that how they lead their organization must change fundamentally.

Steering an enterprise in the Great Transition

Industrialization necessitated new approaches to managing labor, raw material and machinery. The answer was Taylor’s scientific management method. However, this approach does not fit the more complex environment of the Great Transition, where leaders will have to move beyond efficiency and develop ways to evaluate performance that assess the true value of outcomes.

The mathematics of the new economy are not always linear: Feedback loops and tipping points are central to complex systems such as platforms and climate. Insight into complex systems will come from looking forward using models to ask what if, as opposed to looking backwards at reports to ask what happened.

Insight into complex systems will come from looking forward using models to ask what if, as opposed to looking backwards at reports to ask what happened.

Leading teams of people who are diverse in color, gender, social background and sexual orientation will pose difficulties to managers who are used to recruiting in their own image. The challenge will be to recruit not for cultural fit, but for cultural contribution. Further, a control mindset is not suited to the production of intangible assets that depend on soft factors. Managers (is this even the right term?) will have to develop especially strong coaching skills to engage, motivate and retain employees when there is a war for talent. Moreover, team working patterns will have to be designed to establish culture and skills, with space created for observation, feedback and learning by doing.

Since the Great Transition will take decades to play out, the career of any executive today will be defined by change rather than stasis. Customers, competitors and suppliers are all undergoing a comparable transition. What made perfect sense last year may make no sense this year.

Adopting change on the scale and depth of the Great Transition is too big to be driven entirely top-down. So, while leaders must chart the new direction, their greatest contribution will lie in helping others to recognize that a new paradigm provides better answers, asking whether the assumptions that guide daily decisions are shaped by the old industrial paradigm or the reality of the Great Transition.

While leaders must chart the new direction, their greatest contribution will lie in helping others to recognize that a new paradigm provides better answers, asking whether the assumptions that guide daily decisions are shaped by the old industrial paradigm or the reality of the Great Transition.

Mastering information technology is central to the Great Transition

In the economy of the Great Transition, information technology is first and foremost a creator of value to be maximized, and only second a cost to be minimized. Since intangible assets depend on the creative powers and productivity of individuals and teams, the aim will be to boost revenue through giving workers the right tools to augment their internal information processor: the human brain. This goes far beyond enabling remote working. The same level of analysis that has been applied to automation will be required to determine what technology best supports value creation by each worker.

The moment an enterprise starts down the ESG track, it is confounded by missing data. Data on a whole range of new vectors is required, much of it derived from external sources. Data management will need to be overhauled to acquire, synthesize and metabolize this inherently messy ESG data. Furthermore, the ability to explain data and tell stories will become a key skill when decisions must balance multiple aspects of value using qualitative and quantitative data.

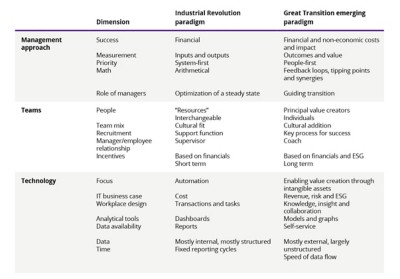

The Industrial Revolution paradigm and the emerging paradigm of the Great Transition are compared in Table 2.

Seizing the opportunities of the Great Transition

By labeling today’s transition a Fourth Industrial Revolution, we are starting from the wrong diagnosis. Through this misdiagnosis, we underestimate both the nature and extent of the Great Transition. As a result, we cannot see the need for, much less adopt, a new paradigm for a new economy.

Once you realize that a new paradigm provides better answers, priorities will inevitably shift from cost to revenue and risk. Profound change in the approaches to leading an enterprise and guiding teams is bound to follow, with information technology recognized as the pivotal lever for value creation.

The Great Transition is not a matter of taste: something to like or dislike. As with the weather, it is just happening. The answer is to embrace rather than resist the Great Transition, seizing its opportunities before your competitors and running ahead of, rather than behind, your stakeholders.